Screenshot

Vivo Energy Kenya blames an uptick in consumption for stock-outs across its Shell network.

But with the government holding 248 million litres in reserves and the Energy CS specifically warning against hoarding — the official story is raising far more questions than it answers.

On the surface, Vivo Energy Kenya’s explanation for empty pumps at several Shell service stations is straightforward: customers are buying more fuel, and replenishment is on the way.

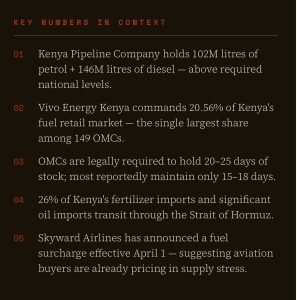

The company, which controls roughly 20 percent of Kenya’s fuel retail market — the single largest share among 149 oil marketing companies — issued a statement on Thursday attributing the shortages to what it called “increased demand” for its products.

It apologised for the inconvenience and assured customers that teams were racing to restock affected sites.

The statement, however, lands in the middle of an uncomfortable context — one that the company’s careful corporate language does not fully address.

Less than 24 hours before Vivo Energy went public with its explanation, Energy and Petroleum Cabinet Secretary Opiyo Wandayi took to the podium with a pointed and unusually direct warning aimed squarely at oil marketing companies (OMCs) like Vivo Energy itself.

“Notwithstanding the stable supply position, we note with concern reports of product hoarding and speculative withholding of stocks. This conduct is commercially opportunistic, contrary to the public interest, and in direct breach of licensing obligations.”— CS Opiyo Wandayi, March 25, 2026

The Cabinet Secretary’s language was unambiguous. The government was not describing a hypothetical risk — it was describing behaviour it said it had already observed.

And crucially, Wandayi confirmed what many suspected: Kenya is NOT facing a supply shortage.

The Kenya Pipeline Company at that moment held 102 million litres of petrol, 146 million litres of diesel, and 1.7 million litres of dual-purpose kerosene — reserves comfortably within national requirement levels.

Timing Problem

The sequence of events here is difficult to ignore. The CS warns on Wednesday that OMCs are speculating on price movements and hoarding stock.

The very next morning, Kenya’s largest OMC announces stock-outs at multiple stations and attributes the gaps to surging customer demand.

The proximity of these two events demands scrutiny that Vivo Energy’s statement does not invite.

What is driving the “surge” in demand? The company has not provided data, historical comparisons, or any granular explanation of where and when this demand spike originated.

Spot checks by journalists tell a more uneven story: diesel ran out at the Kipande House outlet on Monday morning; stations along Magadi Road and in Kiserian had been intermittently dry since Saturday.

That is a pattern that spans several days and multiple locations — not the footprint of a routine weekend rush.

| QUESTION 1

If national reserves hold over 248 million litres, why are Vivo Energy’s own depot collection rates not keeping pace with retail demand? Who controls the pipeline between the Kenya Pipeline Company and Shell forecourts? |

| QUESTION 2

Vivo Energy CEO Peter Murungi initially described the situation as a “long weekend with high consumption.” Is a long-weekend explanation consistent with shortages that began on Saturday and persisted across the week? |

| QUESTION 3

The government says supply systems are “fully operational.” If so, what exactly is preventing Vivo Energy from pulling stock from KPC depots in real time to replenish affected stations? |

| QUESTION 4

OMCs are required to hold 20–25 days of stock, but most reportedly maintain only 15–18 days. Did Vivo Energy enter this period already under its legally required buffer, and if so, why? |

The Speculative Motive

The backdrop to all of this is the escalating Israel-Iran conflict and its effect on global oil markets. The Strait of Hormuz — through which roughly 20 percent of global oil and gas shipments pass — faces real disruption risk.

Iran has warned it could target vessel movement through the narrow channel.

Kenya imports petrol, diesel, and jet fuel on a 180-day credit period from Saudi Aramco, ENOC, and ADNOC under a government-to-government arrangement.

All three Gulf suppliers have reported attacks on their refineries since the conflict widened, raising legitimate concerns about supply continuity.

This is the environment in which a rational, commercially-minded oil company might calculate that fuel prices will rise in the next review cycle.

The Energy and Petroleum Regulatory Authority (EPRA) set current pump prices on March 14 — super petrol at Sh178.28 per litre, diesel at Sh166.54.

The next review will need to account for any global price movements. An OMC holding more stock than it declares at current prices, only to release it post-review at higher gazetted rates, would make a tidy and low-risk margin on the spread.

CS Wandayi has made clear the government will not raise pump prices in response to the current situation.

But the warning itself suggests his ministry believes some companies are betting otherwise — or are at minimum using the uncertainty as cover to restrict supply, watch queues build, and benefit from de-facto higher prices through informal rationing and cash-only payment preferences already reported at some outlets.

KEY NUMBERS IN CONTEXT

| 01 | Kenya Pipeline Company holds 102M litres of petrol + 146M litres of diesel — above required national levels. |